28/05/2026

Validating Market Entry Assumptions with Primary Research Before the Deal Closes

Competitive landscape research that survives an IC vote isn't a database query. It's primary validation of the assumptions in your deal memo. Here's how PE and CDD teams do it before signing.

In commercial due diligence, the most expensive mistakes show the same way. A deal closes on a market thesis built from secondary data. Six months later, the portfolio team discovers that the competitor set on the IC slide does not match the competitor set buyers actually shortlist. The TAM was right. The addressable demand was off by 60%.

That gap, between the landscape you can model from databases and the landscape buyers describe in their own words, is what competitive landscape research is supposed to close. Most of the work that ships at the diligence stage does not close it. This piece walks through what competitive landscape research must do before signing, where it usually fails, and how PE deal teams and CDD consultants run it inside a 48-to-72-hour window.

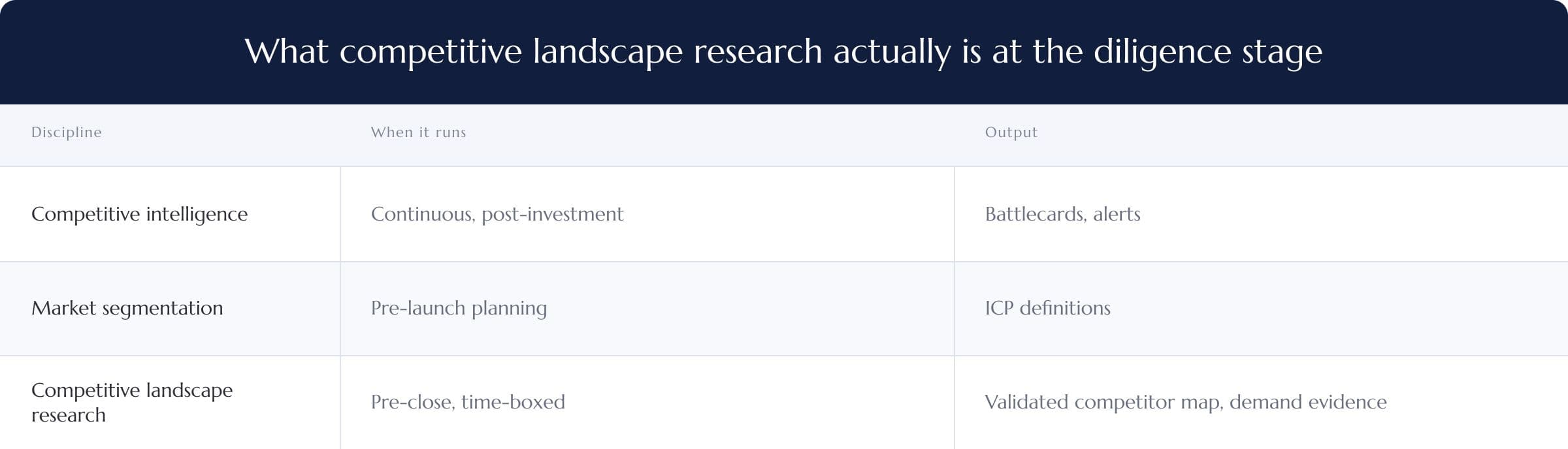

What competitive landscape research actually is at the diligence stage

Competitive landscape research is the structured mapping of who competes for a target's buyers, how those buyers make selection decisions, and which substitutes pull demand sideways. At the diligence stage, it functions as a deal artifact rather than a marketing exercise.

Three terms get used interchangeably and should not be. Competitive intelligence is the ongoing collection of competitor signals once a company is built. Market segmentation is a forward planning exercise on customer groups. Competitive landscape research, in a deal context, is a point-in-time validation of the competitor and demand assumptions the IC memo is built on.

Three components matter pre-close: the actual competitor set as buyers experience it, the substitution map showing what they would buy instead, and live demand evidence for the target's wedge.

Why most landscape research fails to validate market entry assumptions

Three failure modes recur across deals where the thesis later proved wrong. Each comes from over-leaning on secondary data and analyst reports.

Phantom competitors. Filings and review sites surface vendors that buyers do not actually shortlist. CB Insights' analysis of why startups fail puts "no market need" at 35% of failures, the single largest category. The phantom-competitor failure is the inverse problem: you build a defensible position against vendors buyers ignore, and miss the ones doing the displacing.

Stale TAM logic. Most market-sizing in CDD inherits an ICP definition that was current 18 months ago. Buyer roles, budget owners, and procurement paths shift faster than industry analysis reports refresh.

Buyer-substitution blindness. The most consistent gap. Verified buyer interviews surface "if not the target, then X" patterns no database carries, because X is usually a workflow, a spreadsheet, or doing nothing at all. None of those appear in a vendor list.

The assumption ledger: how to structure what primary research has to validate

The assumption ledger is a single artifact built before any interviews start. Every load-bearing claim in the IC memo gets one row. Each row carries the claim, the source it currently rests on, the type of evidence that would disconfirm it, and the cost if it turns out wrong.

An anonymized example from a recent B&H compliance-software CDD: the IC deck claimed the target was the only vendor offering jurisdiction-specific workflow templates for hedge funds and asset managers. That row in the ledger triggered 14 interviews over 48 hours with regulated-fund operations leads across Europe and North America. Three named a competitor offering the same capability under a different brand. The deck got rewritten. The valuation model held, but the differentiation narrative changed.

The ledger forces two things secondary-only diligence never does. It separates claims worth interviewing for from claims already settled. And it puts a price on disconfirmation upfront, which decides which claims get the research budget.

Running competitive benchmarking under a compressed timeline

Compressed diligence windows do not allow for traditional fielding cycles. Bain & Company's own PE client work describes two-week exclusivity periods on tech-led deals. Primary research must land inside that window, or it does not land at all.

Who you interview decides whether the work is decision-grade or theatre. Four buyer types carry the weight: current buyers of the target, ex-buyers who churned to a competitor, lost-deal buyers who evaluated and chose elsewhere, and channel partners with multi-vendor visibility. Cross-border coverage matters when the entry thesis assumes geographic expansion, because buyer behavior in DACH or APAC rarely mirrors the US assumption. Bell & Holmes can run this across 140+ countries and 35+ languages in a single engagement, which most English-source-heavy alternatives cannot match.

What you ask, separates filings from validation. Filings tell you what a vendor sells. A verified buyer tells you what they evaluated against, what tipped the decision, and what would make them switch.

Building the competitive map from the buyer's seat, not the analyst's seat

Most published frameworks on this topic build the landscape from the analyst's seat: filings, review sites, news, web data. That gives you a vendor list. A competitor set is defined by buyer behavior, which is a different artifact.

The data source distinction matters. Platforms like Klue assemble competitor maps from CRM data and review sites. AlphaSense pulls from filings and broker research. Both surface what vendors and analysts say. Neither surfaces what verified buyers say when no vendor is in the room. The buyer-seat map closes that gap with primary interviews, not document mining.

The buyer-seat map answers four questions a database search cannot. Which vendors made the actual shortlist on the last three RFPs in this segment? Which got disqualified at screening, and on what criterion? Which won the deal, and what convinced the budget owner? Which workflow did the losing vendors lose to, often the spreadsheet they were trying to replace?

Constructing the map takes 25 to 40 interviews with verified human buyers across the target's addressable segment. The output is two-sided: a vendor competitive set with shortlist frequency, and a substitution map showing where demand leaks to non-vendor alternatives.

Where business intelligence research sits vs. primary validation

Business intelligence research, including industry analysis and secondary databases, is scaffolding. It tells you where to look, who the named players are, and what the headline trends say. It does not tell you whether the deal thesis holds.

Three positioning gaps only verified-human responses catch: the buyer's actual evaluation shortlist (almost never identical to the analyst-defined competitor set), the unstated reasons a vendor wins or loses deals, and the timing of buyer switching cycles. Platforms surface what vendors say about themselves. They do not surface what buyers say when no vendor is in the room.

The practical rule on a live deal: use business intelligence research to frame the question and pick the interview list. Use primary research to answer the question. That division of labour is why primary fielding has become the default diligence tool, with secondary demoted to scaffolding. Reversing that order, treating BI as the answer, is where most market landscape analysis breaks at the partner meeting.

Market opportunity analysis: sizing the bet, not just the market

Market opportunity analysis at the diligence stage goes beyond TAM math. It measures the addressable demand the target can plausibly capture, net of the substitution and customer-concentration risks an interview round actually surfaces.

McKinsey's M&A practice puts the odds of large-M&A acquirers outperforming industry peers at roughly 50-50, with the differentiator landing in diligence depth and integration discipline. The Harvard Business Review's 2024 analysis by Harding, Shervani and Rovit found that success rates have flipped over the last two decades: today nearly 70% of M&A deals succeed, with primary diligence quality cited as a recurring success factor. Thesis error, when it occurs, still concentrates on the assumptions that secondary data could never have tested.

The decision the opportunity analysis has to support is binary: winning or walking away. A 1,200-respondent panel survey will not tell you the answer in time. A focused 30-interview round, structured against the assumption ledger, usually will, and arrives before the IC vote.

What decision-grade competitive landscape research looks like at the partner meeting

Decision-grade output is what survives a Sunday read by an IC partner who has not been in the weeds. It is short, structured, and built around the assumption ledger, with each high-stakes claim now carrying a status: validated, disconfirmed, or partially supported with specific caveats.

The format that travels: a 6 to 10 slide insight document, an annotated quote bank organized by ledger row, and a one-page recommendation framed as a decision rather than a summary. Best practice on this is restraint. Do not append the full interview transcripts. Put the three quotes per ledger row that change the recommendation, and link the rest.

The test at the partner meeting is simple. Can the principal answer one question per slide without the analyst in the room? If yes, the work is decision-grade. If no, the work is still research.

Bottom line

Most competitive landscape research at the diligence stage is built to look thorough. Decision-grade work is built to be wrong out loud, fast, before the wire transfer.

If you are running a CDD with a closing date in the next four weeks and unvalidated assumptions on the IC slide, Bell & Holmes runs primary research in as little as 48 hours, structured against your assumption ledger. See how we did this on a 30-day Big-4-led CDD with a tight timeline, or get in touch to scope a project.