05/06/2026

The Quiet Shift: Why Primary Research Is Becoming the Default Diligence Tool

Strategy and M&A consulting firms are shifting commercial due diligence from secondary data to primary market research. Here's what changed and what to demand.

A few years ago, primary market research sat in the optional column on most commercial due diligence work plans. You scoped it if the deal had budget and the IC date had give. Today it sits in the required column on almost every CDD we touch for strategy and M&A consulting firms. The shift was quiet, it happened deal by deal, and almost nobody in the market research and consultancy space has named it out loud.

This piece is the buy-side argument for what changed, and what to demand from a research partner when you have three weeks to defend a thesis.

What changed in how strategy and M&A consulting firms buy market research

Three things shifted at once. Deal-cycle clocks compressed. Public-source data converged across AI-search tools, so the "differentiated insight" your team used to pull from secondary research now shows up in every other bidder's deck. And panel quality on B2B respondent samples kept eroding. Together they pushed primary market research from "optional add-on" to the default input layer on commercial due diligence engagements.

For a strategy or M&A consulting firm, that means the question on every CDD intake is no longer whether to commission primary research. It's how fast you can stand it up, how niche the respondent target can be, and how much of the analyst week you protect by handing fielding to someone else.

The global market research industry is on track to clear $93 billion in services revenue this year, per The Business Research Company, and most of that growth is coming from custom B2B work tied to a specific decision rather than from syndicated reports.

Why secondary research stopped being enough for commercial due diligence

Secondary research used to be 70% of the diligence read. It now caps out closer to 30%, with the rest pulled from primary fielding inside the window. There are four operational reasons for this, and none of them are about methodology preferences.

First, public-source convergence. AI-driven search and large-model summarization push the same datasets into every consultant's draft slide — and a significant share of those datasets traces back to fabricated market reports that have spread through AI training data undetected. If your competitive map for a SaaS target reads exactly like the next bidder's, you have not differentiated the thesis.

Second, vendor and customer-side public disclosures have not kept pace with private-market deal velocity, so what's in PitchBook is often two reporting cycles stale by the time you sign the engagement.

Third, the named user base is small enough that you cannot infer adoption from analyst reports on niche targets. You must call the buyers. Fourth, syndicated panels in B2B have a documented seniority-and-verification problem at the decision-maker level, which I'll come back to in the AI section.

What "primary market research" actually means inside a 4-week diligence window

In the consulting context, primary market research means anything where you, or your research partner, generate data directly from named human respondents inside the deal timeline. In practice, that's four tools: B2B in-depth interviews with decision-makers, custom quantitative surveys with verified samples, expert calls for vendor and category context, and targeted secondary triangulation built on top.

Inside a four-week CDD window, the practical split usually lands at 25 to 50 qualitative interviews, sometimes a 200 to 400 respondent quantitative cut where the population supports it, two to four expert calls for category framing, and ongoing desk research as the connective tissue. You don't run all four at scale on every engagement. Your scope is based on the IC question.

What separates qualitative market research services from quantitative on a CDD is the question type: qual answers "why did the buyer switch," quant answers "how many would." Both are decision-cycle tools, framed by the IC question and the calendar rather than by methodology preference.

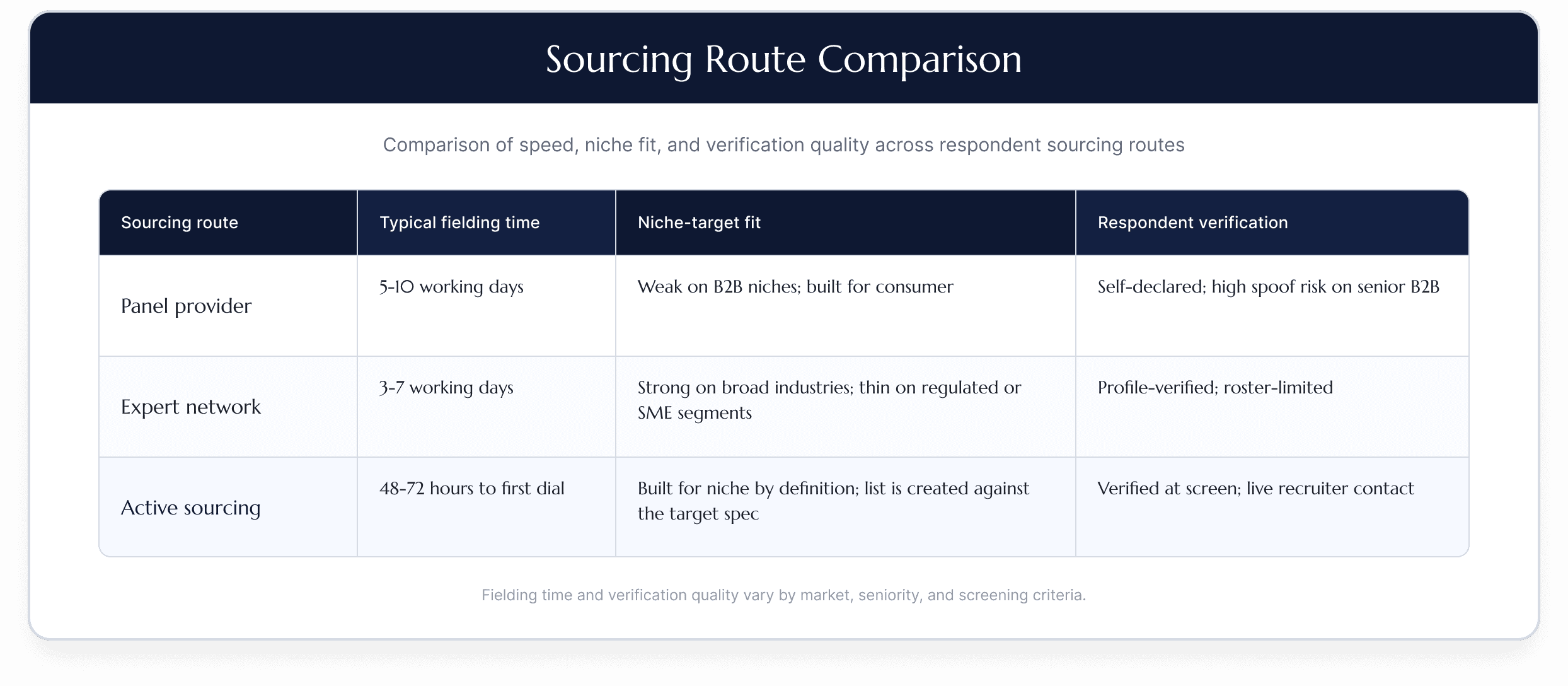

The active-sourcing layer most strategy and consulting firms still outsource

This is the part of B2B market research services that most strategy firms quietly outsource and almost never write about. Panel-based sampling fails on the targets that matter most for CDD: niche compliance software users, county-level public-sector IT buyers, hard-to-reach SME owner-operators, decision-makers at firms that don't show up in any expert-network roster.

Active sourcing means a research team builds the respondent list from scratch against your target spec, screens it in real time, and runs outreach within 48 to 72 hours. On a recent engagement, a UK strategy and technology consultancy was running CDD on a niche compliance software vendor serving hedge funds and asset managers across Europe and North America.

Traditional expert networks could not produce the respondent profile in time. Bell & Holmes ran active sourcing instead, delivering 23 in-depth interviews with C-level compliance, operations, and technology heads across six countries in five working days. The findings shaped the buy-side recommendation while the IC clock was still running.

If you, the deal team lead, have ever burned a Tuesday morning waiting for a panel provider to confirm a 12-respondent screener that should have been turned around in 48 hours, you know exactly what I mean.

When does the panel route still win? Consumer FMCG at scale, brand-equity tracking, multi-market awareness studies. For commercial due diligence on B2B targets, active sourcing has become the default fielding layer.

The operational difference between the three sourcing routes on a tight CDD clock:

Where market segmentation gets sharper when primary data leads

Market segmentation strategies built on firmographic cuts (revenue band, employee count, industry code) are the cheapest segmentation you can do. They are also the least useful for a deal team trying to defend a growth thesis, because every bidder reads the same firmographics off the same Capital IQ pull.

Behavioral segmentation built on primary interviews is what changes the read. You learn that the "mid-market hedge fund" segment actually splits into two segments based on whether compliance reports to legal or to operations, and that the buying committee, switching trigger, and willingness to pay all change at that fork. You only find that out by talking to enough buyers to see the pattern. On a fast-fielded primary study, 30 to 50 well-screened interviews are usually enough to draw the lines with confidence.

Honest excursion: not every diligence needs primary-led segmentation. If the target is a category leader in a mature consumer market and the question is brand share, syndicated tracker data still leads. The primary-led approach pays back hardest on B2B targets in fragmented markets, which is most of the PE deal book in 2026.

How analytics and AI fit into primary-research-led diligence (without replacing it)

Data analytics in market research is genuinely useful inside a CDD window for three tasks: faster transcript synthesis, screener optimization, and survey-data cross-tabbing under deal-team pressure. We use AI-assisted synthesis daily. It saves analyst hours. Analyst judgement still belongs to the analyst.

What AI does not do credibly yet in diligence work is replace the verified human respondent reached through expert-led native-language interviews. Synthetic samples and AI-moderated interviews have a place in pilot-phase consumer research and in screening, where the cost of being wrong is low. Under a fiduciary diligence standard, where the deal team must defend the data to an IC and a fund LP, the chain of custody from "real named decision-maker" to "quoted finding in the slide" matters. That direction of travel is not coincidence.

The operational rule we work to: AI compresses synthesis; humans produce the data. Reverse that order on a $100 million deal, and you are taking a risk that a buy-side IC will not underwrite.

What strategy and M&A consulting firms should demand from a research partner in 2026

If you are scoping a CDD research partner against a tight calendar, six things separate the partners who deliver from the ones who burn your week.

Day-one outreach. The research team starts dialing within hours of brief approval, not after a three-day "internal screener review" cycle. Active sourcing capability for niche targets, not just panel access. Senior researcher delivery, with the same person on the brief call, the screening, and the synthesis. Daily written QC summaries you can paste straight into the project file. Multilingual capability where the target is not US-only - a function of how a firm is actually structured, not just which languages it lists on a website. The remote-first operating model that enables same-day outreach in 35+ languages is meaningfully different from an office-based team that patches in translation support after the brief. And a delivery format you can move into the IC pack with light editing, not a 200-slide PDF that needs rebuilding.

One scoping note worth naming. Buy-side commercial due diligence is not vendor due diligence. CDD answers "is this a thesis we should underwrite," VDD answers "is this an asset we can credibly sell." The respondent target, the question set, and the chain of custody differ. A research partner who has only run sell-side work will write you the wrong screener. Ask which side of the table they have fielded for, and how recently.

A recent diligence we ran for a Big 4 consultancy on behalf of a Private Equity sponsor evaluating a B2B software vendor for SMEs across Europe and North America is a useful checkpoint. The deal had a compressed CDD window, the target was niche, and the Big 4 team needed the primary research layer to land cleanly inside their final deliverable. Bell & Holmes led the primary research component end-to-end. The output dropped into the consultancy's IC pack without rework.

A reasonable counter-example sits inside our own use-case library: a 5-day CDD on the North American ranching sector where the client could not produce a usable contact list at all. The team pivoted to fully independent regional sourcing, delivered 31 interviews with qualified beef and dairy operators inside the window, and the partner-level testimonial reads "we were struggling to get this information, and you were able to get it." That capability is what you should demand from a research partner. Panel access alone will not get you there on a niche B2B target.

For a deeper read on what fielding under this discipline actually surfaces - the patterns that secondary research misses every time - see our companion piece on the red flags that only surface through primary research in due diligence.

There are markets where the primary-research-first thesis genuinely struggles. Multi-quarter brand-equity tracking on consumer categories is one. The syndicated trackers from the global research firms have multi-year time series that no custom fielding can replicate inside a deal window. Regulated industries with mandatory public-comment data are another. The public corpus there is rich enough that primary research is sometimes additive rather than central. And small-population B2B targets where the entire decision-maker base is fewer than 40 people will, by definition, give you thin quant, however hard you field.

If you are sitting on a deal in one of those pockets, primary research still belongs in the mix, though as a layered tool rather than the lead. Primary is not always right. The argument here is narrower: the default position has shifted, and the deal teams still treating primary as the optional layer are working from a 2018 playbook.

The bottom line for diligence-grade decisions

Strategy and M&A consulting firms commissioning commercial due diligence market research in 2026 are buying a different product than they were three years ago. The thesis defense now lives in the primary-fielded layer. The secondary-research slide deck has been demoted to context. The differentiator between research partners is fielding speed, named-target sourcing capability, and the discipline to deliver synthesis the deal team can actually use inside the IC pack.

The shift was quiet. It is also done. The question on the next CDD intake is not whether to scope primary research. It is who you trust to run it on a three-week clock.

If you have a CDD intake coming up that needs primary fielding inside a tight window, the Bell & Holmes team scopes engagements in under 24 hours and starts dialling on day one. No pitch deck, no procurement loop - a working brief and a target spec is enough to get started.