30/04/2026

How to Run Primary Research Under Compressed PE Timelines

Discover how to effectively conduct private equity research under tight timelines. Learn key strategies to enhance your due diligence process.

"The firms that win deals on data don't have more time than everyone else. They have a better research model."

Most private equity teams treat primary research as a confirmatory step - something you do near the end of due diligence to validate what the financial model already suggests. That sequence is backwards. And in a compressed deal cycle, it is actively expensive.

The information asymmetry in PE is not about access to data. Secondary data - industry reports, financial databases, analyst coverage - is widely available. The real gap is between what databases say about a market and what the market's actual participants say when you call them directly. Customer satisfaction scores, ESG performance signals, management track records, and early-warning competitive movements are among the things secondary data handles worst. None of them survive a serious investment committee challenge without primary verification.

Primary research closes that gap. The challenge is doing it fast enough to matter.

Private Equity Research Timelines: Why Setup Determines Outcome

The difference between research that shapes a deal and research that arrives after the decision is rarely about how many interviews get completed. It comes down to when the research function activates in the deal cycle - and whether the operating model behind it can absorb the speed required.

Deal Timing Is a Competitive Variable

Deal timing in private equity is a competitive variable, not an administrative one. A fund that arrives at closing with validated market intelligence holds a negotiating position that a fund still waiting on research does not.

Bain's Global Private Equity Report 2026 documented sustained competitive pressure across mid-market transactions, with increasing buyer competition shortening the interval between exclusivity and close. In that environment, commercial due diligence is not a box to tick after the financial model is done. It is the capability that separates a defensible investment thesis from an expensive assumption. Funds that have pushed primary research earlier in the process - into deal sourcing and pre-exclusivity origination - arrive at term sheets with prior market validation already built into their thesis. That gives them a structural advantage over teams that only start researching after the deal is under exclusivity.

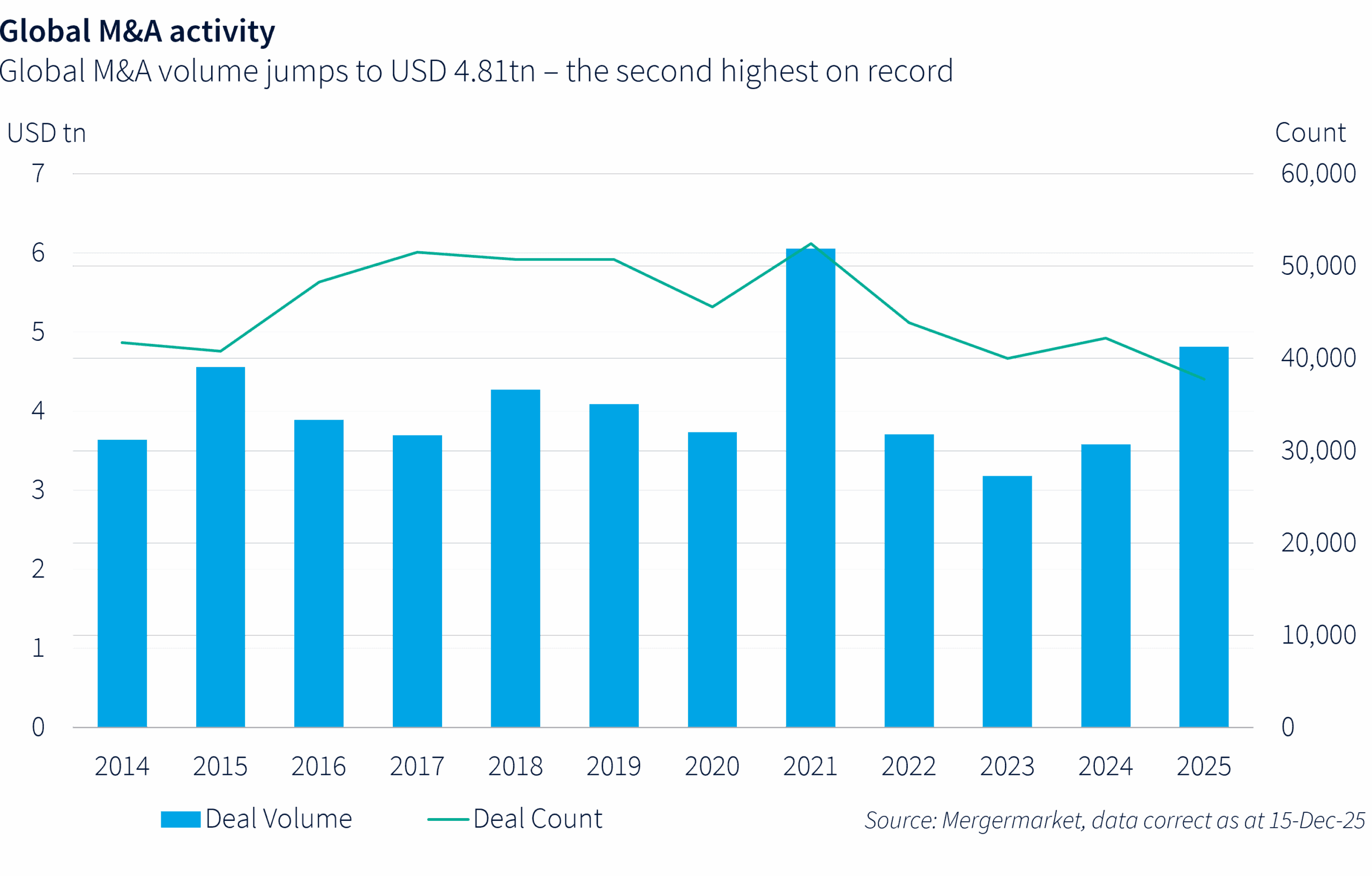

Source: Year of the Megadeals – M&A Highlights FY25, ION Analytics

The CDD Window: From Scoping to Exit

A standard CDD engagement runs five to ten working days - sometimes shorter. That window has to absorb scoping, respondent identification, fielding, synthesis, and delivery - with no buffer for a vendor that needs three days of onboarding before the first call goes out.

The funds that handle this consistently have built the research function into deal prep, not deal close. By the time a term sheet is signed, the research brief is already drafted. And the best-run PE teams do not stop there. The same primary research infrastructure that validates a deal thesis pre-close is equally valuable for post-acquisition - monitoring customer sentiment, tracking competitive movement, and informing exit timing. When a portfolio company's quarterly financials eventually surface a problem, the primary data should have signaled it three months earlier.

Funds that continue primary research across the hold period catch material changes weeks before financial reporting would. When exit timing determines realized returns, that gap between primary signals and lagging secondary data shows directly in valuation multiples. A CIM describes the market from the seller's point of view. Independent primary research - conversations with customers, competitors, channel partners, and former employees - provides the external check that the investment committee cannot get any other way. The funds that consistently outperform build this function into their process from deal origination through exit, not just during the CDD window.

What Compressed Due Diligence Timelines Break First

Time pressure in PE due diligence does not reduce every research component equally. Some areas absorb compression without much damage. Others degrade fast and take the investment thesis with them.

Compressed timelines create two pressure points simultaneously. Scope narrows by necessity - there is no time to investigate every angle. At the same time, the quality bar rises. When the window allows for 15 conversations rather than 50, each one carries more weight.

The first component to get cut is usually management team assessment. Under time pressure, teams reduce reference calls on leadership and redirect that capacity toward customer and competitor volume. That is a costly trade-off. McKinsey's research on PE value creation consistently identifies leadership quality as one of the strongest determinants of whether a thesis actually executes post-close. The financial model may be watertight. A management team that cannot deliver the operational plan it signed up for is the variable that unravels it.

Traditional research providers compound this problem. Expert networks are built for scheduling. A matched expert looks credible on a résumé and can deliver surface commentary in a 45-minute call. Survey panels reach volume quickly but cannot guarantee the respondent behind each submission is who they claim to be. Neither model was designed for PE timelines. Both transfer risk to the research buyer.

Why Secondary Data Fails Under IC Pressure

Speed and quality are not opposites in primary research. They require a different operating model to coexist.

The common failure mode: under time pressure, teams default to secondary sources - a Bloomberg report, a Preqin market brief, an industry association survey. Fast. Available. And backward-looking by construction.

Primary research tells you what the market is doing now. That reversal — secondary demoted to context, primary promoted to the lead input — is now the default position on commercial due diligence, not a methodology preference. A customer satisfaction score in a CIM was accurate when the seller wrote it. Whether it holds after 20 direct conversations with current users is a different question - and the one an investment committee will eventually ask. The specific red flags that primary outreach surfaces - from financial reporting inconsistencies to customer churn signals and competitive positioning gaps - are detailed in Red Flags That Only Surface Through Primary Research in Due Diligence. The same logic applies to ESG. Institutional LPs - pension funds and sovereign wealth funds in particular - now apply ESG screening to fund commitments and expect portfolio-level ESG inputs in reporting. Whether the target's key customers impose supplier ESG requirements, whether the target's practices create regulatory exposure in its primary geographies, whether competitors are building ESG positioning as an active market advantage - none of those questions resolve from a Bloomberg terminal. They require direct conversations with customers, procurement teams, and competitors operating in the same market.

A data gap here does not just affect IC approval. It affects LP relations post-close. And it compounds: the ESG questions an LP asks during fund reporting are the same ones a strategic acquirer will ask at exit. Answering them early, with primary data, builds a defensible position across the entire hold period.

Primary Research for PE: Scoping for Speed

Research quality under compressed timelines depends almost entirely on the specificity of the scoping phase. A loose brief generates days of wasted outreach. A tight brief builds the contact list logically from the research question and gets the first call out within hours of kickoff.

The Four Questions Every CDD Brief Must Answer

Good primary research under time pressure starts with one question: what do we need to know that we cannot get from a database?

In a CDD context, the answer now typically spans four areas, not three. Customer perception of the target - satisfaction levels, switching intent, pricing sensitivity. Competitive positioning - which alternatives actually exist in the market and how they are used in practice. Market trajectory - where demand is heading and what is accelerating or slowing it. And management quality - the track record, decision-making approach, and succession depth of the leadership team, assessed through former employees, industry peers, and references outside the seller's prepared list. That fourth area gets treated as optional under time pressure. It should not be. It is often the one that changes the deal.

A fifth consideration is gaining traction at PE firms with active portfolio programs: exit readiness research. Running targeted outreach to prospective acquirer types during the CDD window - understanding how strategic buyers currently view the category and what operational improvements would raise the target's attractiveness - feeds directly into value creation planning post-close. Each of these areas maps to a distinct respondent type. Defining the objectives first means the contact list builds logically from the brief, not in parallel with it.

Interviews First, Quantitative Validation Second

In a compressed PE timeline, interviews outperform surveys. Not because surveys have no place, but because the questions that matter change as the project progresses.

A structured interview guide is a starting point. Our sample open-ended questions for commercial due diligence show the type of prompts that help fieldwork surface switching, pricing, and retention risks early. By day two, the themes shift. Questions that seemed central at briefing become less relevant. New angles emerge from early calls. A subject matter expert interview guide can follow that. A survey distributed on day one is locked - you cannot adjust it when day three reveals the real issue is pricing structure, not product satisfaction.

Use quantitative instruments to validate themes that have already surfaced through interviews. Run them as secondary confirmation, not as the primary intelligence source.

Technology in Private Equity Research: Contact Pools, Not Shortcuts

Technology has compressed the operational mechanics of primary research. AI-assisted screening, automated dialing systems, and structured note-taking tools reduce the gap between briefing and first call. But the limit of technology in PE research remains judgment - a distinction that defines the human + AI hybrid model now running at the fastest research firms. The tools that matter are more distinct than they appear.

AI Deal Sourcing vs. Proprietary Contact Databases

AI deal sourcing platforms identify private companies matching investment criteria across the market. That is useful at the origination stage. A proprietary contact database that locates specific decision-makers within those companies and enables same-day outreach does something different. The former helps you find targets; the latter lets you call them by end of business. In a compressed CDD window, the second capability determines whether research starts on day one or day three.

When Bell & Holmes ran a three-day strategic research project for a European private equity firm evaluating an enterprise data platform, 16 in-depth interviews with heads of data and IT directors were completed across North America and Scandinavia - precisely because the contact pool existed before the brief arrived. The client's PE partner described the turnaround as "higher than expected" for both volume and depth within the timeline. Build contact pools fast. Apply human judgment to work them.

Synthesis Built for the IC Slide Deck

Synthesis under compressed timelines does not benefit from complex NLP platforms that take longer to configure than the project itself. The most effective approach is a consistent tagging framework applied during fielding: sentiment classification, theme tags by research area, and a confidence score per interview.

That structure makes it possible to deliver a working synthesis within hours of the final call, not days after it. For investment committee use, the synthesis format matters as much as the content. Structured summaries mapped directly to deal thesis questions, with verbatim quotes ready for slides and confidence scores attached to each key finding, are significantly more useful to a deal team than a narrative report that requires internal reformatting under deadline.

Competitive Landscape Research: Testing Market Position from Outside

Validating market entry assumptions in a PE context serves one purpose: confirming that the target's market position holds when tested from the outside, not just as described in the seller's materials. The questions that surface real competitive risk are behavioral, not descriptive.

Do customers actually consider alternatives? What would prompt them to switch? How long has the competitive set been stable? McKinsey's research on PE value creation consistently identifies market structure - competitive intensity, switching costs, customer concentration - as among the strongest predictors of deal performance. That data does not live in a market report. It surfaces in a conversation with a customer who tried to leave and didn't, and can explain why.

ESG is increasingly a competitive benchmarking dimension in B2B sectors with institutional procurement teams. The question is not whether the target has an ESG policy. The question is whether customers actively weigh it in purchase or renewal decisions, and whether competitors are using ESG positioning to erode the target's standing. Three customers naming the same new entrant unprompted is a competitive signal that no analyst report captures in real time. A market trend that looks like a clear tailwind in a secondary research report can look very different after 20 direct conversations.

Comparable Deal Evidence Strengthens the Thesis

Real-world private equity case studies from comparable deals are underused in PE primary research. They serve two purposes: calibrating research scope and providing reference points for investment committee presentations.

A fund that can show its thesis survived the same scrutiny that revealed problems in a comparable situation is telling a more credible story to its LP base. In a recent CDD engagement for a Big 3 consultancy evaluating niche compliance software used by hedge funds and asset managers, Bell & Holmes completed 23 in-depth interviews with C-level executives and compliance heads across six countries in five working days - with multilingual outreach across Italy, the Netherlands, France, the UK, the US, and Canada. The findings shaped the consultancy's advisory recommendations directly in the active deal process. The same research capability has supported hedge funds entering sectors where PE has previously worked and credit funds conducting pre-lending due diligence in overlapping verticals - the underlying method transfers; what changes is the respondent set and the thesis framing.

PE Due Diligence Consulting at Big 3 Speed

When a Big 3 or Big 4 firm manages the CDD process on behalf of a PE fund, the research vendor relationship becomes time-critical from minute one. Consulting teams need a research partner who can scope and start without a week of onboarding - and who can run independently between check-ins rather than waiting for direction.

Consulting teams do not work in 48–72 hour blocks. They operate on a daily evidence cycle, where priorities shift every 24 hours and answers are expected by the next morning. The cadence that works in these engagements is simple: morning alignment on what matters now, fielding throughout the day, and structured synthesis delivered the next morning. That rhythm requires infrastructure built for speed, flexibility, and continuous output.

Research defensibility has become an explicit IC requirement, not just a methodological preference. Investment committees regularly challenge data sourcing during CDD presentations - not the conclusions, but the mechanics. Whose responses are these? How were respondents identified? Can this data hold up if an opposing adviser challenges it? Transparent sampling logic, and documented sourcing protocols have moved from footnotes to deal-critical inputs. Research that cannot answer these questions clearly does not survive IC scrutiny.

In a CDD engagement for a Big 3 consultancy covering agricultural markets across three continents, Bell & Holmes delivered 30+ interviews in five working days with native-language outreach across the US, UK, France, Spain, Italy, and India - a project where the client could not join daily calls and relied entirely on written synthesis and structured daily summaries to steer priorities.

What Separates PE Research Firms from General Agencies

Specialized private equity research firms exist for exactly this pressure point. The distinction from a general market research agency is operational infrastructure: pre-built contact pools in relevant sectors, research consultants trained in cold outreach who can reach hard-to-access respondents at deal speed, and quality assurance processes that flag low-confidence interviews before they affect the dataset.

The sourcing model matters more than most CDD teams realize. Expert networks recruit opt-in members who have registered on a platform and are available for scheduled calls. Cold outreach targets respondents based solely on relevance to the research question - no platform affiliation, no prior relationship with the research firm. An unaffiliated respondent who takes a cold call and commits 20 minutes is a fundamentally different data point: independent, unprimed, and not associated with the vendor's existing network. When verified human respondents with documented sourcing are what the IC table requires, the operating model behind the research is the product - not a process detail.

For funds running four to eight transactions per year - and increasingly for credit funds and hedge funds applying the same primary intelligence standard to pre-lending and pre-investment decisions - this infrastructure is what keeps the research function competitive.

Conclusion

The constraint in primary research under compressed PE timelines is rarely time itself. It is setup. Teams that define objectives tightly - covering customers, competitive positioning, management quality, ESG exposure, and exit readiness - prioritize respondent quality over sample volume, and partner with vendors built for deal-cycle speed will consistently produce better investment intelligence than those who wait for more data or settle for secondary sources.

The research function that wins at the deal table can get a verified, unaffiliated, decision-relevant respondents on the phone by end of business on day one - and deliver a synthesis the IC can use by end of business on day five. Every other variable is secondary.

Bell & Holmes runs primary research for PE Investment Directors and Big 3 consulting teams on 48-hour timelines. Research Consultants operate across 140+ countries and 35+ languages, delivering human-verified interviews that hold up in front of an investment committee. If you have a deal in motion, contact Bell & Holmes or see how this works in practice before the window closes.