17/07/2026

Sample Open-Ended Questions for Commercial Due Diligence: A Practitioner’s Template

Sample open-ended questions for commercial due diligence, organised by investigation area, plus how to probe, analyse, and turn answers into deal-grade findings. A practitioner’s template.

Search “due diligence questions” and you get checklists asking who owns the company, whether the tax returns are clean, and where the IP sits. Useful for your lawyers. Useless for the question that actually decides the deal: is this market real, and will these customers still be here in three years?

That answer does not live in a data room. It lives in the heads of the people who buy, sell, switch, and churn in the target’s market, and the only way to get it out is to ask them well. An open-ended question in qualitative research is one that cannot be answered with “yes,” “no,” or a number on a scale. It invites the respondent to answer in their own words, which is where the reasoning, the hesitation, and the red flag you did not know to look for tend to surface.

None of this makes interviews the answer to every question. When the target’s own cohort data already tells you retention is holding, a survey confirms it faster and cheaper than a round of calls. Open-ended interviews earn their cost on the questions the numbers cannot settle: why customers stay, what would make them leave, and whether the growth story is real or borrowed. Use them there, not everywhere.

This is a working template. Below are sample open-ended questions organised by the areas a commercial due diligence actually needs to test, how to tell a strong answer from a weak one, and how to turn a stack of transcripts into a finding your investment committee will accept. If you are mid-fieldwork and just want the questions, skip straight to the question bank.

Why open-ended questions decide the deal, not just the dataset

Closed questions confirm the thesis you walked in with. Open questions surface the one you missed. That difference is measurable, and it is larger than most deal teams assume.

The Pew Research Center ran the cleanest demonstration of this in its November 2008 post-election survey. Respondents were asked what one issue mattered most in deciding how they voted for president. Asked in a closed format, 58% picked “the economy” from the list. Asked the same question open-ended, left to write their own answer, only 35% said anything the coders could file under “the economy,” and 43% of responses fell into “other,” a category that had drawn just 8% in the closed version. The list did not measure opinion. It manufactured it.

That is the exact failure mode of a diligence built on closed questions. Hand a target’s customers a satisfaction scale and most will circle a 7 and move on. Ask them to describe the last time the product let them down and you learn whether the 7 is loyalty or inertia. As Converse and Presser noted in their 1986 SAGE volume Survey Questions, closed formats push respondents toward the answers the investigator already had in mind, while open formats reveal what is actually top of mind. In a deal, top of mind is where the risk hides.

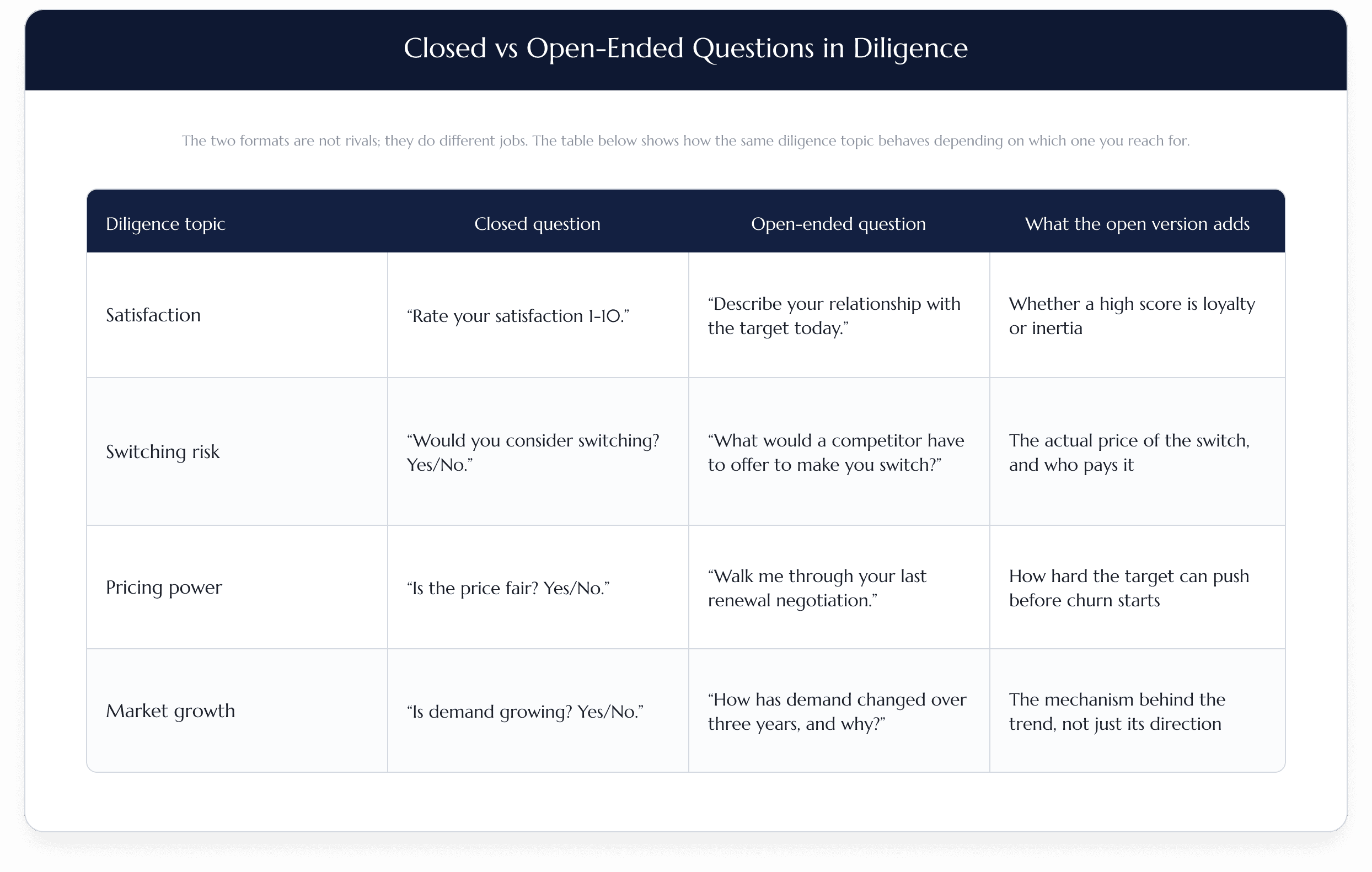

The two formats are not rivals; they do different jobs. The table below shows how the same diligence topic behaves depending on which one you reach for.

Use closed questions to size and rank once you know what to measure. Use open questions first, to find out what you should have been measuring. A diligence that skips the second step tends to confirm the deal thesis on the way in and discover the flaw on the way out.

What makes an open-ended question work in a diligence interview

A good open-ended question is neutral, singular, and specific to the respondent’s own experience. It does not lead, it does not stack two questions into one, and it does not ask people to speak for their whole company when you want their personal view.

Start broad, then funnel. Open a topic with something the respondent cannot answer in a word (“Walk me through how your team chose your current provider”), then narrow toward the detail you need (“What would have to change for you to switch away from it?”). Phrasing the opener as a command, “Tell me about,” “Walk me through,” “Describe,” tends to draw a longer, less guarded answer than a question that starts with “Do you.”

Framing matters more than most interviewers think. Ask “When your company evaluates suppliers…” and you get the official procurement line. Ask “When you last evaluated a supplier…” and you get what the person actually did. Werk Insight makes the same point in its B2B qualitative guide: anchor the question to the individual buyer’s experience, not the company’s policy, or you get a bureaucratic, surface-level answer that tells you nothing you could not have read in a brochure.

One caution before the bank. Open-ended does not mean unlimited. Some survey research points to response quality dropping off sharply once a respondent faces more than four or five open-ended items in a row. In a live diligence interview you have more room than a survey does, but the principle holds: a tight set of well-aimed open questions with real follow-up beats a long list asked mechanically.

Sample open-ended questions for commercial due diligence

The questions below are grouped by the investigation areas a commercial due diligence has to cover. Treat them as a bank, not a script. Pull the five or six that map to your deal thesis, and leave room to follow the answers where they go.

Market attractiveness and growth

Competitive position and switching

Customer retention, churn, and satisfaction

Pricing power and willingness to pay

Management quality and operational risk

Red-flag probes

That last question earns its place on its own. It hands the respondent the pen, and in diligence after diligence it is where the answer you could not have scripted arrives.

What a strong answer looks like

A strong answer is specific, first-hand, and reasoned. A weak answer is general, second-hand, or a single adjective. The gap between the two is closed by the follow-up, not the opening question.

Here is the same exchange run two ways. The opener is identical: “What keeps you with [target] rather than a cheaper alternative?” Weak, left alone: “They’re reliable. We’ve been with them a long time.” That is a 7 on a scale dressed up as a sentence. It tells you nothing about whether the relationship survives a price rise or a champion leaving.

Strong, with one probe: “They’re reliable. We’ve been with them a long time.” → “Tell me about a time that reliability was tested.” → “Last year our integration broke the night before a board reporting deadline. Their support lead stayed on with us until 2am and had a workaround by morning. Our previous vendor would have opened a ticket and gone home. That’s the whole reason we renewed without shopping around.”

Same respondent, same question, ninety seconds apart. The second answer is a retention thesis you can underwrite. Cascade Insights calls this the power of the follow-up, and the mechanics are simple: when an answer is broad, short, or drifting, you clarify, you connect back to something said earlier, or you ask for the specific instance. You keep pulling until the answer is concrete enough to defend in front of an investment committee.

Turning transcripts into a defensible finding

Once the interviews are done, the questions have done their job and the analysis begins. The goal is to move from dozens of individual answers to a small number of themes you can stand behind. This is where thematic analysis earns its keep.

Thematic analysis is a structured way of reading qualitative data. You code each transcript by tagging passages with what they are about (“price sensitivity,” “switching trigger,” “support quality”), then group the codes into themes, then check the themes against the full dataset to make sure they hold. Done properly, qualitative data analysis produces a claim like “nine of twenty-three customers named the same support engineer as their reason for renewing,” which is a finding, not an impression.

Walk it through once. Say twenty-three customers each answer “what keeps you with the target rather than a cheaper alternative?” You tag the transcripts: eleven passages get “support responsiveness,” nine get “switching cost too high,” six get “no real alternative exists,” four get “contract lock-in.” Group those codes and two themes dominate: the retention story is built on service quality and on the absence of a credible competitor, not on price or contract terms. That is a finding an investment committee can act on, and a very different one from “customers seem happy.” It also tells you exactly what to stress-test next: if the support engineer everyone named leaves, does the retention thesis survive?

How many interviews do you need?

Enough to reach saturation, and rarely more. Two disciplines keep the analysis defensible. The first is saturation. Some research puts typical qualitative samples at 5 to 30 participants for interviews, with saturation reached at the point where new interviews stop producing new themes. If your last four interviews told you nothing the first nineteen had not, you have enough. The second is triangulation: cross-checking a theme against more than one source or method before you rely on it, so a single vocal respondent does not become the finding on their own.

A note on sample size in diligence specifically. The academic ranges assume a leisurely study. Deals do not grant that. Bell & Holmes routinely runs well above the textbook numbers inside a single week, 23 verified interviews across six countries on one compliance-software diligence, 105 on a US trucking engagement built from a client list that turned out to be unusable. Volume is not the point on its own. Enough of the right respondents, reached fast, is what lets you claim saturation honestly rather than hoping for it.

Three ways good questions still fail

The questions are the easy part. Most diligence interviews that come back thin fail for one of three reasons, and none of them is the wording of the opener.

The first is talking to the wrong person. A beautifully phrased question aimed at someone two rungs below the actual decision-maker returns confident, useless answers. Screen for the person who signs, switches, or vetoes before the interview counts, not after.

The second is accepting the first answer. The bank above is a set of doors, not a set of destinations. A respondent’s opening reply is almost always the rehearsed version; the diligence-grade answer is one or two follow-ups behind it. An interviewer who works a list top to bottom without probing will fill the sheet and learn nothing.

The third is asking the company’s view instead of the person’s. “How does your organisation evaluate suppliers” gets you the procurement policy. “When you last evaluated a supplier” gets you what actually happened. The moment a question invites someone to speak for the org rather than themselves, the answer flattens into something you could have read on their website.

Running these interviews under a compressed timeline

Most guides to qualitative interviewing assume you have weeks. In commercial due diligence you have days, sometimes a long weekend, and the compression changes how you run the questions rather than which questions you ask.

You keep the structure semi-structured: a fixed spine of open questions so every interview is comparable, and enough flexibility to chase the red flag when it appears. You verify who you are actually talking to before the call counts, because a diligence finding is only as defensible as the respondent behind it, and “a senior person at a competitor” is worth nothing if you cannot show they were the real decision-maker. In practice that means confirming the person’s current role, employer, and buying authority against an independent source before the interview is logged, not taking a panel’s word or a broker’s profile at face value. A survey panel cannot show you that; an expert network hands you a name but rarely proves the seat is still theirs. And you go to the respondent in their own language when the target’s market is not English-speaking, because a hedged translation is where nuance, and risk, quietly disappears.

This is also where the interview approach separates from the two alternatives a deal team usually reaches for. An expert network sells you access to a handful of pre-vetted names on a call-by-call basis, filtered through a broker and priced by the hour; more often than not, you get depth, but slowly, narrowly, and at one remove from the target’s actual customers. A survey panel sells you scale, but hands you closed-question data that confirms rather than discovers. Running the open questions yourself, at speed, gets you the depth of the first without the filter and the reach of the second without the flattening.

Speed is where the method usually breaks and where it does not have to. On the diligences behind this template, our teams delivered inside five to seven working days across North America, Europe, and Asia, in the respondents’ native languages, with daily written summaries so the deal team could steer while fieldwork was still live. One Big 3 partner, on the trucking engagement, put it plainly after we reached a population their own channels could not: “This was an excellent piece of work and critical to our project.”

From question list to deal-grade insight

A question bank is a starting point, not an outcome. The template above will get you better raw material than a generic survey ever will. What turns that material into a call your investment committee accepts is the execution around it: the right respondents, verified; the follow-up that converts a rehearsed answer into a reason; the analysis that survives scrutiny; and the speed to do all of it before the deal moves without you. The same discipline underpins the interviews behind an expert-witness engagement, where a testimony-grade finding has to hold up under cross-examination, not just in an investment memo.

That is the line between winning the asset and walking away from it, and it is decided in the interviews, not the data room.

If you have a live diligence and a compressed window, Bell & Holmes runs the primary research behind commercial due diligence for private equity and consulting teams, in 140+ countries and 35+ languages, with verified human respondents and a 48-hour standard on delivery. Start a scoping conversation, or see how the compliance-software diligence behind this template came together in five working days.

Article Q&A

What are five examples of open-ended questions? Five that work in any diligence interview: “Walk me through how you chose your current provider.” “What would make you switch away from it?” “Describe the last time the product let you down.” “How has demand in this category changed over three years?” “What are you not being asked that you think matters here?” Each one is impossible to answer with a single word, and each invites the reasoning behind the answer.

What is an open-ended question, and how does it differ from a closed one? An open-ended question cannot be answered with “yes,” “no,” or a point on a scale; it asks the respondent to reply in their own words. A closed question offers a fixed set of responses to pick from. Closed questions are faster to count; open questions surface the reasoning, the exceptions, and the risks a fixed list never anticipated.

What are examples of qualitative research questions for due diligence? Group them by what the diligence needs to test: market growth, competitive position, retention and churn, pricing power, and management quality. The question bank above gives five to eight for each area. The pattern is consistent: anchor the question to the respondent’s own experience (“when you last…”) rather than their company’s policy (“how does your organisation…”).

How many open-ended questions should one interview include? Fewer than instinct suggests. Some survey research shows response quality falling once a respondent faces more than four or five open-ended items in a row. A live interview gives you more room than a survey, but the principle holds: a short set of well-aimed questions with real follow-up beats a long list read mechanically.