07/07/2026

What Is a Red Flag Review — and Why PE Firms Are Running Them Earlier

A red flag review is a fast, focused due diligence check PE firms run early to catch deal-breakers before full CDD. Here's what it covers and why timing matters.

You have signed the NDA, the teaser looks clean, and the banker wants indicative bids in ten days. You do not yet know whether the target's three largest customers are about to re-tender, whether the growth in the model is real demand or a pricing artefact, or whether the market is quietly consolidating around a competitor. That gap between what the data room shows and what the market knows is exactly what a red flag review is built to close, before you commit real diligence spend.

A red flag due diligence review is a fast, focused screen that hunts for deal-breakers first. It does not try to value every line of the business. It works through four questions, and each one changes what you do next: does anything here move the value, force a change to the deal structure, affect the timing, or kill your appetite to bid at all? Get those answers early and the rest of the process runs cleaner. Get them late and they cost you.

What a red flag review is in a PE transaction

A red flag review is a condensed diligence exercise that identifies the risks capable of derailing a transaction, then rates them by severity so a deal team can act. RSM, one of the transaction-advisory networks that publishes on the format, describes the output as a report that flags "threats that may prevent a transaction from being successfully completed" with a structured quantification of each risk, typically rated low, medium, or high, or shown as green, amber, and red.

The deliverable is the "red flag report" itself: a short document that groups issues by category, rates each one, and points to the evidence behind it. In a private equity context, the categories that matter are rarely just accounting entries. They are commercial: is the demand durable, are the top customers loyal, is the competitive moat real, is the growth story defensible under questioning.

That is the difference worth holding onto. Financial, legal, and tax red flags come from reading the target's own documents. Commercial red flags do not, and that distinction runs through the rest of this article.

What red flags does a red flag review look for?

A red flag review scans for the specific issues most likely to break a deal, grouped by category. Most of them come from the target's own records. A smaller, decisive set only surfaces when you talk to the market. The split matters, because it tells you which flags a desk review can find and which it will miss.

Financial red flags (found in the documents):

- Divergent cash flow: profits that look strong on paper but sit alongside negative operating cash flow.

- Accounting irregularities: sudden changes in accounting method, missing data, or unexplained restatements that flatter the figures.

- Unfunded liabilities: hidden pension or post-retirement obligations, or unrecorded tax exposure.

- High debt or unresolved tax liabilities that constrain the deal after close.

Legal and structural red flags (found in the documents):

- Unresolved litigation: pending lawsuits, product liability claims, or regulatory investigations.

- Complex or opaque ownership: multi-layered or offshore structures that can conceal conflicts or illicit flows.

- Expiring or non-transferable contracts and change-of-control clauses that let a key customer or lender walk on a sale.

- Missing corporate records: incomplete board minutes, share registers, or articles of incorporation.

Commercial red flags (found only in the market):

- High customer concentration: an outsized share of revenue tied to one or two accounts. Benchmark International, an M&A advisory firm, names this as one of the most common red flags, and Google's own AI Overview for this topic lists it too. The document tells you the concentration exists. Only the customer tells you whether they are about to leave.

- Churn risk and demand durability: whether the growth in the model is real, repeatable demand or a pricing artefact about to unwind.

- Competitive erosion: whether the moat the thesis assumes is actually holding, or quietly consolidating around a rival.

The first two groups are what accounting firms, law firms, and data-room reviews are built to catch. The third group is the one that most often blows up a deal after close, and it is the group a desk review structurally cannot see. These are the red flags that only surface through primary research.

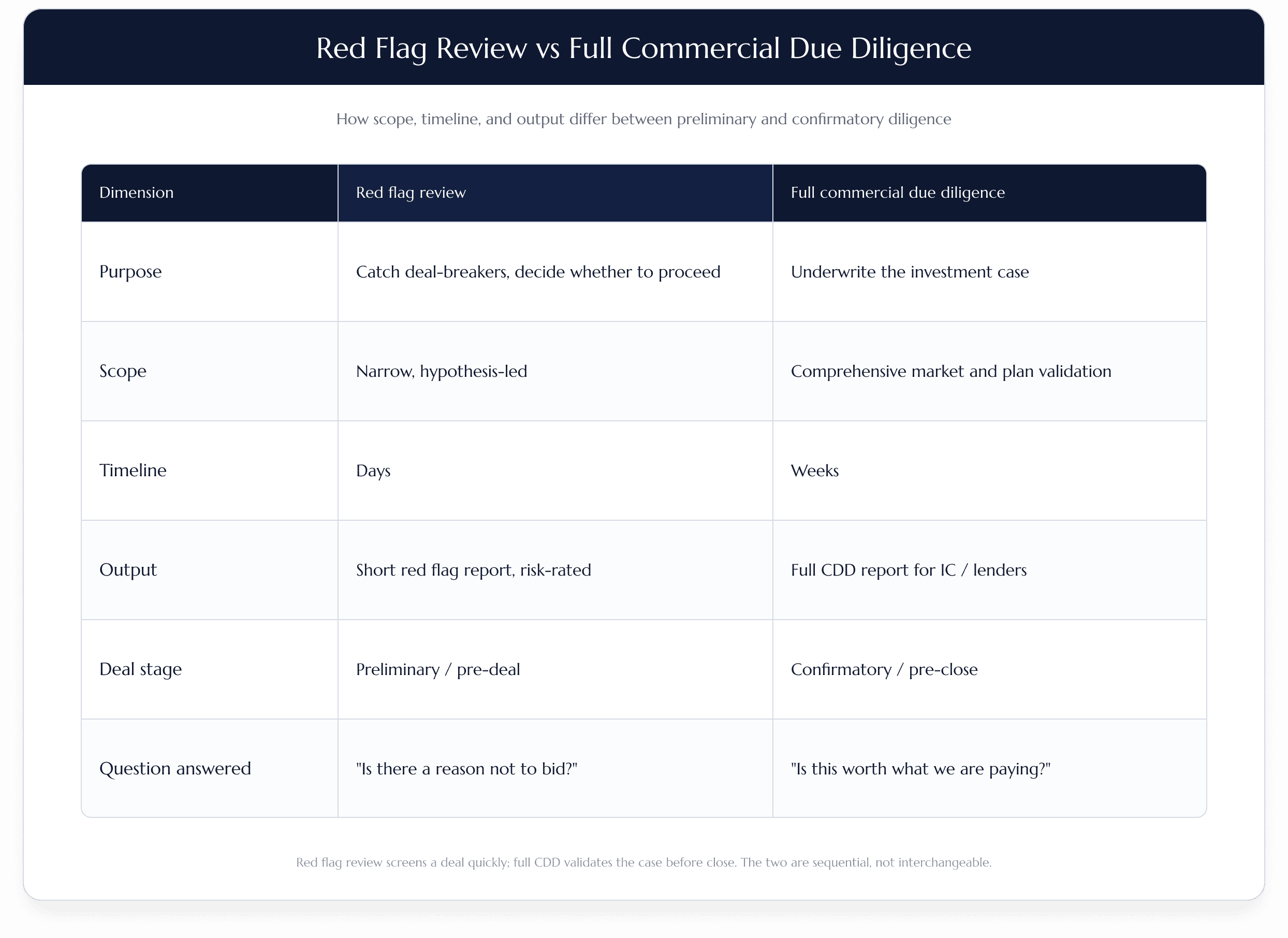

How a red flag review differs from full commercial due diligence

Full commercial due diligence is exhaustive. It builds the market model, sizes every segment, stress-tests the plan, and produces a report a lender or investment committee can underwrite. A red flag review is the opposite instinct: narrow, fast, and decision-led. It exists to tell you whether full CDD is even worth commissioning.

The two are sequential, not competing. RSM sets the ordering out plainly: a red flag report and a draft report belong at the initial stage of a deal, while the final and confirmatory reports come later, at negotiation and closing. Preliminary work catches the deal-breakers; confirmatory due diligence, run once sensitive data is finally disclosed, verifies the detail. Running the cheap screen first is what protects you from paying for the expensive one on a deal that was never going to clear.

The point of the red flag stage is triage. You are not trying to be right about everything. You are trying to be sure there is no single issue big enough to walk away from before you spend the diligence budget and the partner hours that full CDD demands. A red flag review runs at a fraction of the cost and timeline of full commercial due diligence, which is the whole economic case for doing it first: you risk a small, fast spend to avoid committing a large, slow one to a deal that was never going to clear.

Why PE firms are running red flag reviews earlier in the deal process

Deal processes have compressed. In competitive auctions, sponsors are asked for a view before the data room is fully populated, sometimes before management access is granted. Waiting for full CDD to surface a problem now means waiting until after you have already put a number on the table. That is too late to be cheap.

Running the screen earlier changes the economics of a bad deal. If a red flag review kills a process in week one, you have spent days, not weeks, and you have freed the team to work the deals that can actually close. The Dynegy–Enron collapse is the textbook case: Dynegy abandoned its roughly $10 billion merger in 2001, invoking the material-adverse-change clause after fresh information about Enron's trading position came to light, and Enron filed for bankruptcy within days. Its chairman, Chuck Watson, put it bluntly at the time, telling The Guardian: "Sometimes a company's best deals are the ones they did not do. We knew when to say no." The value was in the walk-away, and the walk-away depended on finding the flag in time.

There is a second driver, and it is about appetite. Early signal tells a partner not just whether a deal is clean but whether it is worth the fund's attention at all. In a market where deal teams are stretched across more processes than they can properly staff, a fast read on "is this real" is a triage tool for the pipeline, not just the transaction.

How early red flag reviews spot issues affecting value, structure, timing, and appetite

A good red flag review is organised around four decisions, not a generic risk checklist. Each one changes what you do next.

Value. If the growth in the model rests on customers who are lukewarm, or on a price point the market is already resisting, the number on the page is wrong. Customer and channel interviews surface that before it is baked into your bid. A law firm reviewing contracts can tell you a customer is concentrated; only the customer can tell you they are unhappy.

Structure. Some red flags do not kill a deal, they reshape it. A change-of-control clause that triggers loan repayment, a subsidy that lapses on acquisition, an unassignable key contract: these push the deal toward an asset structure, an escrow, or a specific indemnity. Robbins DiMonte, an M&A law firm, lists contract assignability and customer concentration among the issues that most often force renegotiation rather than collapse.

Timing. A pending regulatory decision or a contract up for renewal in the diligence window can mean the right deal at the wrong moment. Knowing that early lets you sequence the bid around it instead of being surprised by it.

Appetite. Sometimes the honest output is that the deal is fine and still not for you: the market is softer than the thesis assumed, or the upside needs heroics. Surfacing that in week one is a gift, not a failure. It is the difference between a disciplined pass and an expensive maybe.

Why red flag reviews reduce late surprises and support better bid discipline

The most expensive surprises are the late ones. A problem found the week before signing forces a scramble: re-price under time pressure, renegotiate from a weak position, or pull out after sinking real cost into the process. SoftBank's experience with WeWork is the cautionary version. As The Guardian reported, SoftBank paid almost $1.5 billion to WeWork's lenders, including Goldman Sachs, less than a week before the company filed for bankruptcy in 2023, the tail end of an investment that eventually exceeded $16 billion into a business whose lease-heavy model and governance problems had been visible for years. Diligence that arrives that late no longer shapes the decision; it just documents one already made.

Early red flag work does the opposite. It puts the worst news at the front of the process, when you still have every option: bid lower, bid conditionally, restructure, or walk. That is what bid discipline actually means in a competitive auction. Not bidding less, but bidding on the basis of what the market told you rather than what the seller's deck asserted. In an auction, the firm that has already pressure-tested the demand story can move faster and more confidently than the ones still hoping full CDD comes back clean.

How Bell & Holmes runs red flag reviews

The gap in most red flag work is the commercial side. Accounting firms read the financials, law firms read the contracts, data rooms store the documents, and all of it is desk review of what the target chose to disclose. None of it hears from the market.

Bell & Holmes runs the primary research layer: fast, targeted interviews with the customers, former customers, competitors, and industry experts who actually know whether the demand story holds. We are not a panel or an expert network reselling the same rolodex. We source and screen respondents to the specific question, verifying that each one is a genuine decision-maker or user rather than a sales rep or a name on a list, in native language where the market needs it, across more than 140 countries. In a red flag review that screening is the difference between a real churn signal and a reassuring anecdote from the wrong person.

This is where the commercial red flag gets tested. On a Big Four-led CDD for a private equity buyer assessing the acquisition of a B2B software provider in a fragmented, regulated SME market across Europe and North America, the documents and the Big Four workstream could describe the target, but they could not confirm whether the demand and growth story held. To assess commercial viability and growth potential, the PE firm commissioned primary research, and we led that component under the deal's compressed timeline. The question the data room could not answer, whether the market actually wanted what the target was selling, is the one that only the market can answer.

Speed is the point. On another commercial due diligence, for a global consultancy validating market interest in a niche compliance solution, we delivered 23 in-depth interviews with C-level decision-makers across six countries in five working days, and the findings fed directly into an active diligence process. That is the tempo a red flag review needs: signal in days, formatted for the partner meeting, not a month later.

If you are weighing a bid and need to know whether the commercial story survives contact with the market, a short scoping conversation is the fastest way to find out what a red flag review would cover on your specific target.

Talk to us about a red flag review →

If you want the wider argument for why primary data increasingly drives the best private-market deals, we make the full case separately.

Article Q&A

What are the red flags of customer due diligence? In a commercial context, the customer-side red flags are concentration, churn risk, and eroding satisfaction. A single account carrying an outsized share of revenue, key customers quietly evaluating alternatives, or renewal conversations going cold are the signals that most often undercut a growth thesis. None of them appear reliably in the data room. They come from interviewing the customers directly.

What are the top 3 red flags in a deal? Across most transactions, three do the most damage: high customer concentration (revenue tied to one or two accounts), unresolved litigation or regulatory exposure, and accounting irregularities such as strong paper profit alongside negative operating cash flow. The first is commercial and needs market evidence; the other two sit in the documents.

What are some red flags that would trigger enhanced due diligence (EDD)? Enhanced due diligence is usually triggered by opaque or multi-layered ownership, offshore structures, politically exposed parties, or unexplained fund flows, anything that suggests conflicts of interest or compliance risk. A red flag review flags these early so the deal team can commission the deeper background and legal work before committing to full diligence.

What are the 4 P's of due diligence? A common framing is People, Performance, Position, and Prospects: the quality of management, the financial track record, the competitive position in the market, and the durability of future demand. A red flag review is the fast first pass across all four, designed to catch a deal-breaker in any one of them before full CDD begins.